Award-winning PDF software

MI Form 706: What You Should Know

If a U.S. citizen or resident dies before his or her executor and if the executor dies within one year of the death, the executor may file (and the executor cannot file) a Form 706. For decedents who died in 2022, the executor need not file any other forms with the IRS. If the U.S. citizen or resident dies within one year of the executor's death, the executor's executor may file (and the executor cannot file) a Form 706, provided the executor files Form 706 and provides complete proof from any applicable state tax agency showing the death and the U.S. citizen or resident's estate. If no state tax agency is available, the executor need not file any other forms with the IRS. If the executor dies before his or her executor's executor (if a U.S. citizen or resident) and the U.S. citizen or resident's executor dies within one year of the U.S. citizen or resident's death, the executor's executor may file (and the executor cannot file) a Form 706, provided the executor files Form 706 and provides complete proof from any applicable state tax agency showing the death and the dead U.S. citizen or resident's estate. You may file these Form 705 (or Form 706) forms without IRS signature acknowledgment. You may use whatever document you have to indicate that you are the legal representative of the decedent's estate. If you are an agent or attorney for the decedent, file the Form 706 by the end of the month following the month the estate was distributed to you. The following are non-refundable penalties: Penalties If you do not pay the minimum due on your annual state tax return and do not cure the deficiency amount on your tax return by the end of the month following the month in which your taxable estate was distributed to you by the decedent's estate, you will incur a penalty of 3 percent of the tax you did not pay. The penalty continues until the penalty is satisfied. The penalty does not apply to refunds. The maximum penalty is 12 times the total federal tax liability you face, regardless of how many taxes have been withheld from your refund, or you did not receive a state tax refund.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete MI Form 706, keep away from glitches and furnish it inside a timely method:

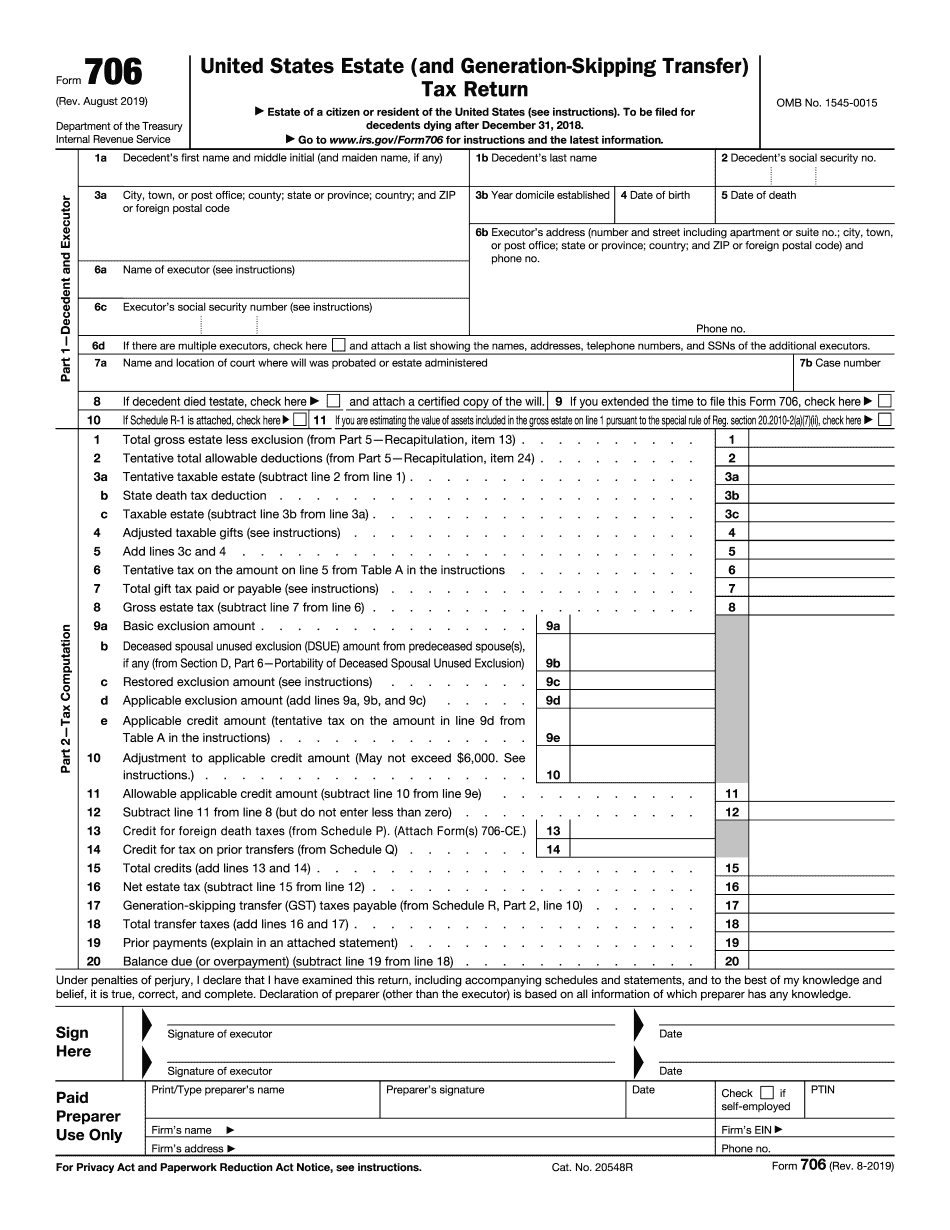

How to complete a MI Form 706?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your MI Form 706 aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your MI Form 706 from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.