Award-winning PDF software

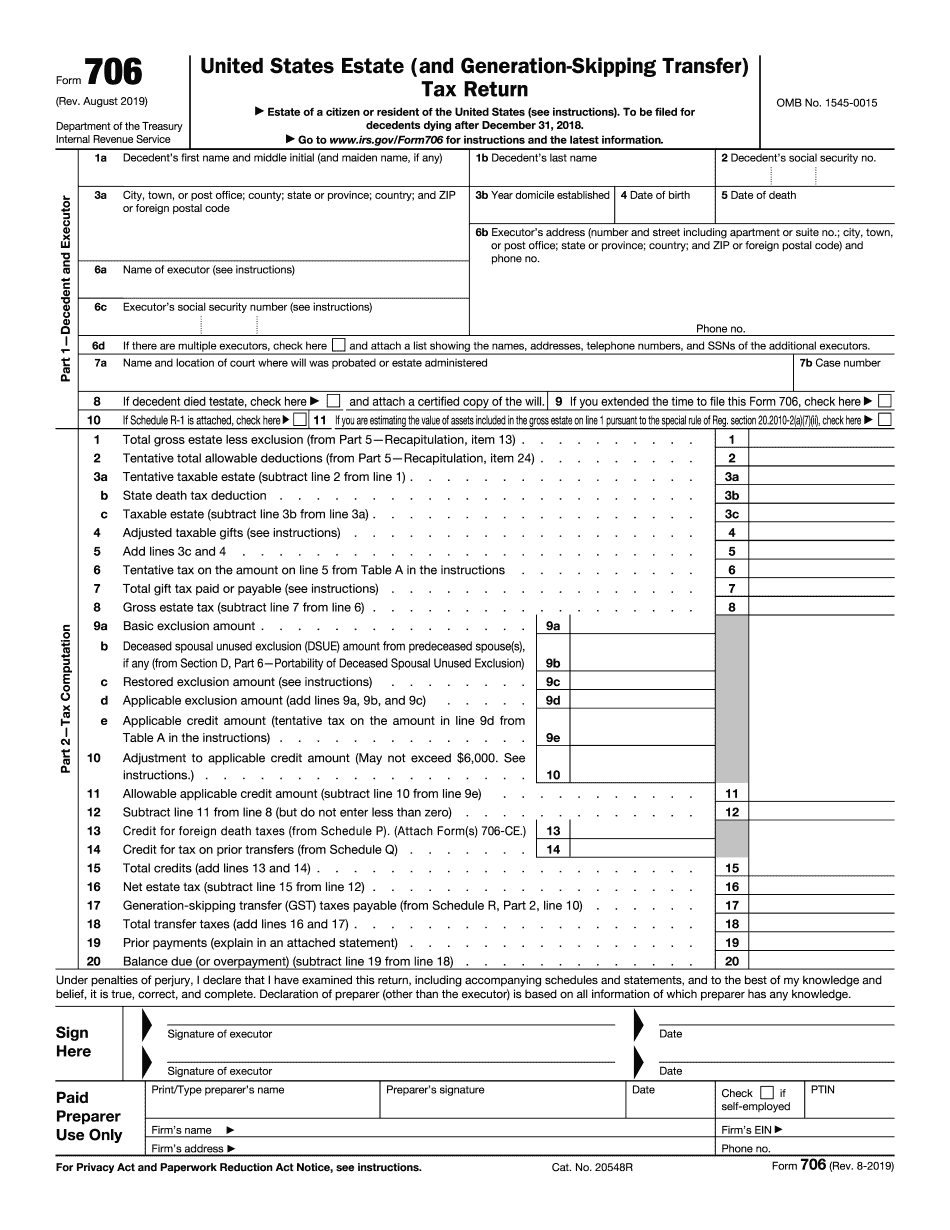

ID Form 706: What You Should Know

This is also called the “final return”. For a taxpayer to determine this date, subtract the payment due date from the date of death. This number is your final return date. The most common situations for a final return are: · When the income attributable to the decedent is greater than the income includible in the estate tax return. In this case, the IRS will calculate the “gross estate income”. The gross estate income is the estate taxes due plus the value of the property not subject to the Estate Tax. · The decedent left no survivors. This means the estate must distribute these assets before the last survivor dies. · The executor or administrator must pay the full amount of the federal gift tax, gift income tax, capital gains tax, and estate tax. · If the executor or administrator is subject to tax on the remaining estate, including the federal estate tax, the final estate tax payment date also counts as the last day. When a final return is due, the executor or administrator must send the estate a final return form. The final return form must be sent within thirty (30) days of the date the executor or administrator determines the estate tax liability and, if applicable, file the correct federal Form W-4 with the IRS. If the executor or administrator decides to wait for a Form W-3, they must mail a copy of the original final return to the IRS, if no original Form W-4 has been filed. A second copy of Form W-4, completed in the following manner, must be sent to: · the IRS, address: Internal Revenue Service PO Box 26150 Washington, DC 20 After a final return is due, the executor or administrator must keep a copy of the estate tax documents received. The executor or administrator must mail this copy of the documents, with the final estate tax return, along with the final return, within thirty (30) days of the close of business or, in the case of a corporation, within thirty (30) days of the filing of final tax returns for the estate of the deceased. The executor or administrator must also mail any payment received under the estate tax to the IRS, as required if taxes have been unpaid. The following instructions will help executors and administrators complete Form 706: 1.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete ID Form 706, keep away from glitches and furnish it inside a timely method:

How to complete a ID Form 706?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your ID Form 706 aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your ID Form 706 from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.